Yields Are Back, but Could Rise Further

Yields are back. For those with a long-term horizon who can withstand some near-term bumps in the road, it’s an exciting time to be an investor and position portfolios for potential upside. But in the short-term, we foresee potential price downside in domestic fixed income and even higher yields before the skies clear.

Key takeaways

Two key risks could challenge recent market optimism: weaker consumption and a squeeze on corporate profitability.

Despite these elevated risks, current credit spreads are not reflective of recessionary risks when compared with historical levels.

The opportunity set for income remains compelling over the long-term, but we believe the time to go all-in on risk assets has not yet arrived given this disconnect.

It’s true. Yields are back. For those with a long-term horizon who can withstand some near-term bumps in the road, it’s an exciting time to be an investor and position portfolios for potential upside. But in the short-term, we foresee potential price downside in domestic fixed income and even higher yields before the skies clear.

Today, there are two key risks that could challenge the recent optimism reflected in risk assets: one related to the growth outlook, the other related to corporate profitability.

On the growth front, the US consumer could be in for a rough patch. After surging throughout the Covid period, consumer spending on goods remains elevated and well above the pre-pandemic trend, as the chart below shows. So much so that the US Personal Savings rate is down to 40-year lows at 2.4% vs. a long-term average of 7.4%, according to Bloomberg as of November 2022. If consumer spending dries up, this could have an outsized impact on GDP growth and could ultimately lead to a hard landing scenario.

At the same time, regardless of whether we find ourselves in a recession, corporate profitability is challenged. Wage inflation was over 6% at the end of 2022, according to the Atlanta Fed Wage Growth Tracker. Conversely, Core Goods inflation has been decelerating sharply. There is a mismatch between the pace at which company prices are falling vs. how quickly their input costs (namely wages) are rising. Said another way, money earned by businesses is declining rapidly while money spent remains stubbornly high.

The disconnect between economic risks and asset prices

Despite an overall challenging year for markets in 2022, risk assets staged an impressive rally in the fourth quarter and the start of this year. While there are developments worth rejoicing over, most notably peaking inflation and China re-opening, we remain skeptical that markets adequately reflect the twin risks noted above.

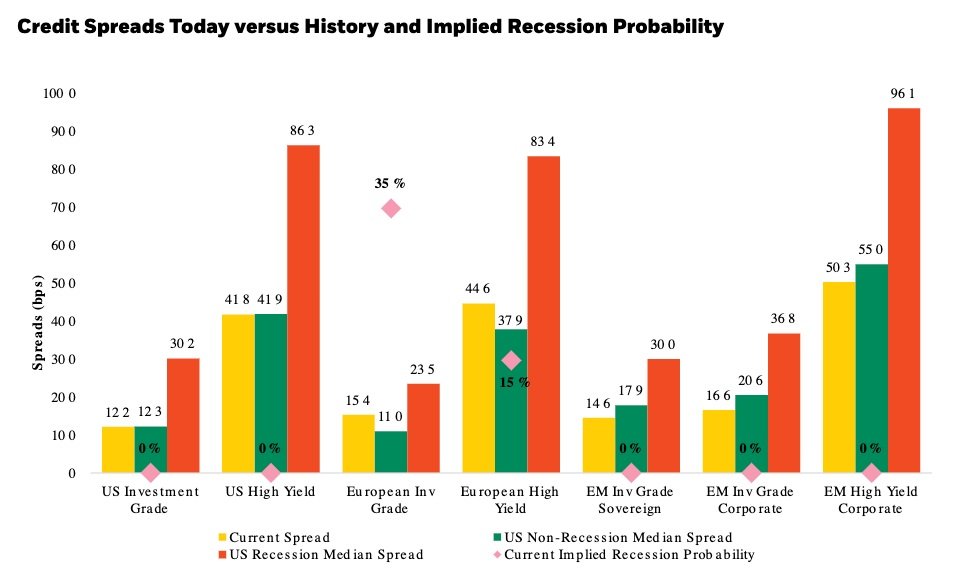

Take US high yield bonds as an example. We looked at credit spreads today against those during recent recessionary periods (e.g., Global Financial Crisis and 2020 Covid drawdown) as well as non-recessionary periods. As shown in the chart below, compared to history, current spreads are much closer to non-recessionary median levels than recessionary median levels – implying virtually no probability of a recession.

In other words, if we were to experience a more meaningful growth downturn or profitability squeeze – which is quite possible, in our opinion - there is significant room for credit spreads to widen from current levels. A similar phenomenon has occurred in US investment grade, Emerging Markets, and, to a lesser extent, European credit markets. Meanwhile, equity risk premiums are also tracking similarly to historical non-recessionary levels.

Source: Bloomberg, BlackRock. 9/17/2002-1/23/2023. US Investment Grade represented by the Bloomberg US Corporate Bond Index. US High Yield represented by the Bloomberg US High Yield 2% Issuer Capped Index. European Investment Grade represented by the Bloomberg Euro Aggregate Corporate Index. European High Yield represented by the Bloomberg Euro High Yield Bond Index. EM Investment Grade Sovereign represented by JPM EMBI Global Diversified Inv Grade Sovereign Spread Index. EM Investment Grade Corporate represented by JPM CEMBI Broad Div High Grade Spread to Worst Index. EM High Yield Corporate represented by JPM CEMBI Broad Div High Yield Spread to Worst Index. A basis point (bps) is one hundredth of one percent (e.g. one basis point = 0.01%). Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Bringing it all together

The opportunity set for income remains compelling, but the time to go all-in on risk assets has not yet arrived, in our view. As such, we have been leaning into lower-risk, higher-quality fixed-income assets that offer attractive yields, upside potential after last year’s weakness, and downside protection in a risk-off event.

Should markets start pricing in more meaningful recession risk, these high-quality positions can act as dry powder to put to work elsewhere. Equally, we’re optimistic on dividend stocks, where the cash flow can provide some stability versus more volatile growth stocks. At the end of the day, staying diversified and nimble are of the utmost importance in navigating today’s still uncertain climate.