Does Investing In European Equities Still Make Sense?

The tragic war in Ukraine has led to an indiscriminate sell-off in European equities. While headlines weigh on sentiment, the 1Q earnings season was strong for Europe.

At the start of the year, the outlook for Europe looked bright as a result of expected economic acceleration due to a surge in services spending once the Omicron wave faded, as well as the rebuilding of inventories as supply chain stresses slowly improved (especially in autos). This easing of supply chain issues, combined with an easier base of comparison for energy prices, was expected to reduce elevated inflation levels after the first quarter. European corporate earnings and markets were expected to outperform U.S. ones, given that cyclical sectors represent over half of its market capitalization. In addition, longer term, the greater fiscal integration of countries within the block, born out of pandemic necessity, but persisting beyond it (EUR800bn NextGenerationEU loan and grant program), was expected to lead to better growth and lower political risk.

Since the turn of the year, the long-term outlook remains unchanged, but the short-term one has darkened considerably. The tragic War in Ukraine has hit Europe particularly hard given its dependency on Russian natural gas (causing European prices to surge to historically high levels), as well as its auto industry’s reliance on key inputs from Ukraine for its supply chain. Currently, the question is not whether the region is eking out positive growth (the June flash Eurozone Composite PMI of 51.9 is consistent with about 1.5% GDP growth), but whether consumer and business confidence is deteriorating enough to land the region in a recession in the second half of the year. Confidence indicators have tumbled since Russia’s invasion, with June consumer confidence nearly eclipsing its historical low hit in April 2020. In addition, the Composite PMI future output index has seen a steep fall to the lowest level since October 2020, with particular weakness in manufacturing. Thus far, current activity has been supported by solid corporate and household balance sheets, a record low unemployment rate and fiscal transfers from national governments; however, short-term risks continue to build, most recently due to concerns not only about the price but also the supply availability of natural gas.

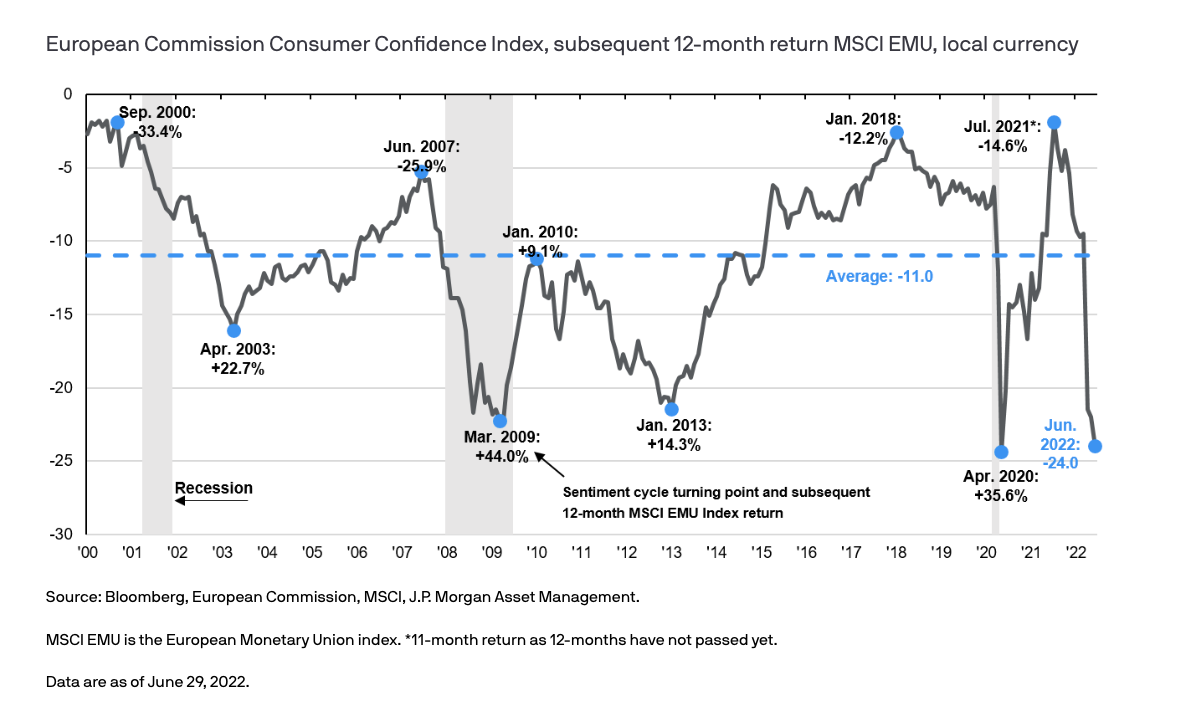

The tragic war in Ukraine has led to an indiscriminate sell-off in European equities. While headlines weigh on sentiment, the 1Q earnings season was strong for Europe. Compared to the U.S., Japan, and EM, Europe had the highest beats on earnings, sales and margins, and the highest earnings and sales growth (aggregate and median company). Forward consensus earnings estimates have risen robustly in Europe as other regions have been flat to down. As markets reconnect with fundamentals, this presents opportunity. Historically, low sentiment in Europe (such as today) has coincided with strong future long-term returns (on average 29% over the next twelve months following a sentiment trough).

Three key reasons to not ignore the opportunity in European equities:

While recession fears in Europe are elevated, investing in Europe is not a bet on the European economy. In fact, over 50% of Europe's revenue comes from outside its borders. For example, LVMH (French-listed, global luxury brand) sources revenue from all other the world, with over 40% coming from EM, where there is growing demand from the rise of the middle class.

Most consider Europe as a cyclical play, but it also represents structural growth opportunities. European markets experienced a significant change in sector composition since the Global Financial Crisis. Looking at the Euro Stoxx 50, financials dominated the index at ~35% of market capitalization in 2008, dropping to under 15% today. Meanwhile, technology has risen from 6% to over 20% of the index. This share is expected to grow further with 20% of the EUR750 billion European recovery fund allocated to digitalize economies.

Investing in Europe offers exposure to opportunities not available in the U.S. Europe dominates the luxury goods space and is at the forefront of the energy transition. 75% of offshore wind capacity is installed in Europe. The EU is focused on phasing out its dependence on Russian oil and pushing forward with the "REPowerEU Plan.” This plan will cut EU dependency of Russian oil by two thirds by the end of 2022 and entirely by 2030.

Sentiment troughs tend to be followed by strong future market returns