The Rebirth of American Manufacturing: Growth and Innovation

While manufacturing activity in the U.S. has largely been in structural decline since the late 1970’s, the makings of a manufacturing renaissance may be starting to emerge.

Key Takeaways

While manufacturing activity in the U.S. has largely been in structural decline since the late 1970’s, the makings of a manufacturing renaissance may be starting to emerge.

Structural trends stemming from the mega force of geopolitical fragmentation could be driving this manufacturing renewal, including reshaping supply chains to emphasize resilience and changing political and economic priorities.

Potential investment opportunities exist across the entire U.S. manufacturing value chain ranging from U.S. manufacturers themselves, to peripheral industries such as auto makers, defense contractors, and construction.

A Manufacting Renaissance Begins

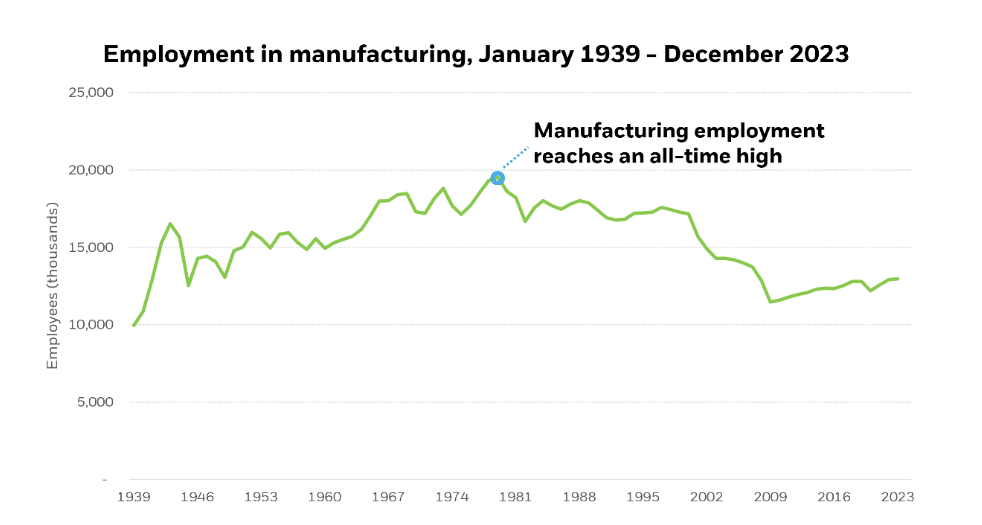

In 1979, U.S. employment in manufacturing peaked at nearly 20 million workers1. Over the next 45 years, manufacturing entered a structural decline and trough as the U.S. transitioned towards a more service-oriented economy. This shift has been pervasive, impacting everything from national output and household consumption to the number of businesses and employees. By 2020, the service sector dominated the U.S. economy, contributing a staggering 79% to GDP, up from 52% in 1950, and representing 80% of total employment2. Concurrently with this rise, the production of goods was increasingly transferred overseas to countries with ample low-cost labor forces.

Chart Source: U.S. Bureau of Labor Statistics, 2024 Manufacturing Jobs, https://data.bls.gov/pdq/SurveyOutputServlet

Chart Description: Line chart depicting manufacturing employment from 1939 to 2023, highlighting the year 1979 when the workforce reached its peak

While the period from the end of WWII through the global financial crisis saw greater global economic integration as labor, goods and information traveled more freely around the world, a series of developments have now cast doubt on the continuation of this trend. Brexit, the COVID-19 pandemic, and war in Eastern Europe have shown that globally integrated supply chains can expose economies to geographic and political risks.

In an era with new economic drivers like artificial intelligence and electrification, governments and businesses alike are looking to accelerate and lead in these key industries and mitigate supply chain risks. As a result, governments and companies are now working to build more supply chain resilience, with reshoring playing a key role. Reshoring is the process of bringing production or manufacturing back to the country of origin.(Learn more about reshoring in our Thematic Mid-Year Update).

Companies with a focus on manufacturing in the U.S. may stand to benefit from this theme of reshoring as tax incentives, tariffs, government contracts, and business preferences may improve the economics of manufacturing goods in America.

Shortening Supply Chains to Build More Resilience

The pandemic highlighted how impactful supply chain risks can be. Take semiconductors for example. Semiconductors are one of the most globally integrated supply chains with 88% of semiconductor production occurring overseas3, and a single chip crossing as many as 70 international borders in production before its end-use4. Before the pandemic, the lead time for semiconductors was three to four months. However, between 2021-2022, this wait period ballooned to a year or more5. Given the widespread use of semiconductors from automobiles to kitchen appliances, disrupted supply chains caused many industries to slow or grind to a halt.

A similar story unfolded in a post-covid world with raw materials such as lumber, where limited availability led to delays in home construction and renovation projects. These bottlenecks prompted a deep dive review of supply chain issues. As a result, the Department of Defense flagged concerns regarding 37 critical minerals, noting that more than half of global production is reliant on a single country6.

A high concentration of supply from one geographic region could pose economic risks, whether caused by a pandemic, changing geopolitical relationships, or other exogenous factors.

Bipartisan Support for Domestic Manufacturing Resulting in Policy Tailwinds

Beyond attempting to de-risk supply chains, supporting the revitalization of U.S. manufacturing may be a favorite among politicians across the political spectrum. Manufacturing contributes over $2.35 trillion to the U.S. economy, representing 11% of GDP, and has the highest multiplier effect of any sector—each dollar spent on manufacturing triggers a chain reaction of increased material purchases, job creation, and further economic expansion7.

Recent U.S. government policies have implemented both a carrot and stick approach to catalyze more domestic manufacturing. The carrot: over $2.1 trillion has been allocated to pro-manufacturing initiatives including the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS and Science Act8. These policies are designed to accelerate the buildout of domestic infrastructure and manufacturing capabilities in key industries and incentivize more investment from the private sector. As of November 2023, the private sector has pledged an additional $614 billion towards the production of semiconductors, electric vehicles, and batteries9.

Chart Source: Deloitte, "Executing on the $2 trillion investment to boost American competitiveness," 03/16/2023

Chart Description: Bar chart showing the $USD amount invested in different manufacturing initiatives including the Infrastructure Investment and Jobs Act, Inflation Reduction Act, CHIPS and Science Act

The stick: over the last eight years the government has taken additional steps to increase the competitiveness of the U.S. and its key trade partners through increased tariffs and both import and export restrictions on key technologies like semis and electric vehicles. Tariffs have increased by almost 85% from 2014-202210. These measures are designed to increase trade barriers in critical industries and protect U.S. economic interests. Together, this carrot and stick strategy could give a significant boost to U.S. manufacturing and position it as a key potential beneficiary of these policies.

U.S. Manufacturing is Gaining Steam

Early signs that manufacturing activity in the U.S. is picking up are emerging – from more construction spend, to hiring, and corporate interest. As of May 2024, annual construction spending in manufacturing soared to $234 billion, tripling since January 202011.

Chart Source: Federal Reserve Bank of St. Louis, “Total Construction Spending: Manufacturing in the U.S., https://fred.stlouisfed.org/series/TLMFGCONS

Chart Description: Shaded line chart depicting U.S. manufacturing spending from 2018 to 2024, highlighting that spending has tripled since January of 2020.

The job market may be following this construction boom. Since early 2021 to date, there have been over 750,000 new manufacturing jobs created12. Due to evolving demand, the industry is projected to create 3.8 million new job openings by 203313.

Top executives at corporations have been focused on reshoring as well. In the first quarter of 2023, mentions of reshoring in S&P 500 earnings calls more than doubled to 128% compared to the previous year14. Altogether, rising manufacturing, hiring, and corporate focus on reshoring could mean manufacturing activity may increase in the U.S. in the coming years as new factories come on-line.

Conclusion

After nearly four-decades, U.S. manufacturing has been showing signs of a resurgence driven by geopolitical shifts and a focus on supply chain resilience. Factors such as reshoring initiatives, government policies supporting domestic manufacturing, and increasing corporate investments have been contributing to this turnaround, leaving U.S. manufacturing poised for possible expansion in the years ahead.

Potential investment opportunities exist across the entire U.S. manufacturing value chain By taking a broad thematic approach to investing in U.S. manufacturing, investors can potentially access exposure to companies that could be poised to benefit from U.S. legislation incentivizing more domestic manufacturing, alongside peripheral industries such as auto makers, defense contractors, and construction.

Investors interested in this trend may consider a targeted ETF, which could be used in place of traditional sectors such as industrials or as a satellite position to complement a diversified core, such as the iShares U.S. Manufacturing ETF (MADE), or an actively managed ETF that can potentially capture the themes of U.S. manufacturing and reshoring, such as the BlackRock Large Cap Value ETF (BLCV) which is actively managed by Tony DeSpirito and the BlackRock Income & Value Team.