Market Perspectives August 2021

The state of the global economy at midyear still very much depends on the course of COVID-19, especially considering differences in vaccination rates and varied levels of fiscal support.

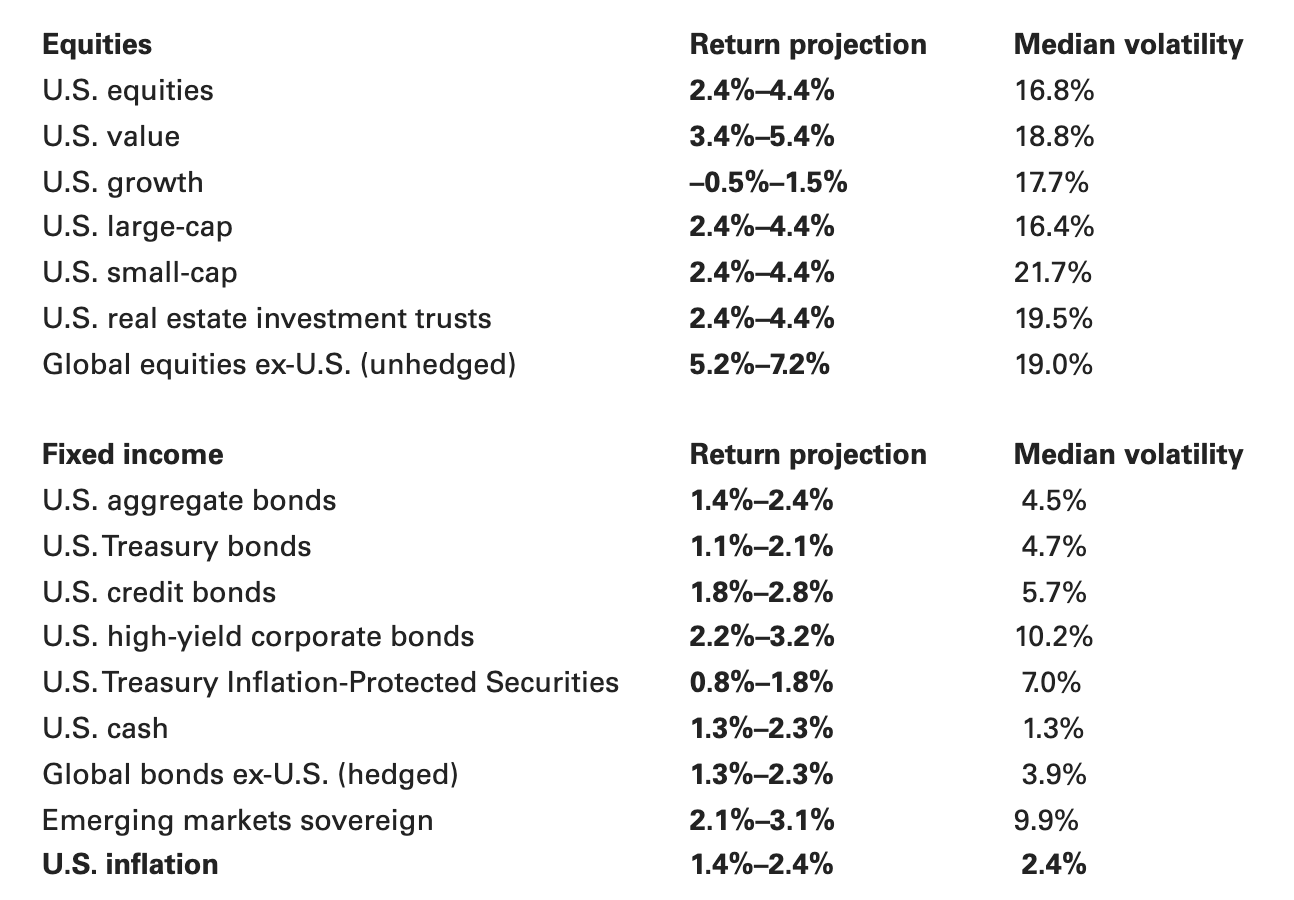

Asset-class return outlooks

Our 10-year, annualized, nominal return projections are shown below. The bolded figures reflect a May 31, 2021, running of the Vanguard Capital Markets Model® (VCMM) for broad equity and fixed income asset classes only. Outlooks for U.S. sub-asset classes reflect a March 31, 2021, running of the VCMM. Please note that the figures are based on a 1.0-point range around the rounded 50th percentile of the distribution of return outcomes for equities and a 0.5-point range around the rounded 50th percentile for fixed income.

These probabilistic return assumptions depend on current market conditions and, as such, may change over time.

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from the VCMM are derived from 10,000 simulations for each modeled asset class. Simulations are as of March 31, 2021, and May 31, 2021. Results from the model may vary with each use and over time. For more information, see the Notes section.

Source: Vanguard Investment Strategy Group.

Growth outlook will vary based on the course of the pandemic

The state of the global economy at midyear still very much depends on the course of COVID-19, especially considering differences in vaccination rates and varied levels of fiscal support.

We expect the path to economic recovery to be uneven and varied across industries and countries, with countries that have vaccinated greater proportions of their populations driving global growth.

Vanguard foresees the United States (with its strong fiscal support) and China (the first to emerge from pandemic restrictions) will lead the way.

United States

In the United States, positive health care developments and strong fiscal support are driving growth. Vaccination programs accelerated after a somewhat slow start, paving the way for the reopening of segments of the economy that depend heavily on face-to-face interaction. Government programs, including enhanced unemployment benefits and stimulus checks delivered directly to lower-income earners, have supported consumer spending.

The first estimate of second-quarter GDP in the United States by the U.S. Bureau of Economic Analysis (BEA) is likely to show strong growth, though perhaps below the double digits that some market participants may expect. Vanguard looks for the pace of growth to slow in the second half, though remain strong as positive health outcomes drive a broader reopening of the economy.

We continue to foresee full-year growth of at least 7%, with activity likely peaking late in the second quarter and early in the third.

Euro area

High-frequency indicators, including aggregate purchasing managers' indexes near 15-year highs, support Vanguard's view that growth in the euro area hasn't yet peaked. We expect that peak to occur in the third quarter, and we continue to anticipate that the region will experience full-year growth around 4% to 5%.

We expect the recovery to be led by a substantial rebound in consumption in the coming months. The global economic recovery, meanwhile, is supportive of export growth in Germany and Italy.

Vanguard believes euro area GDP will reach its pre-pandemic level in the first quarter of 2022.

China

Growth momentum in China has faded in recent months in response to tighter fiscal and monetary policy and slowing export growth. We expect support from the export sector to wane and consumption growth to normalize slowly, given sporadic virus outbreaks and an initially slow vaccination rollout.

China's composite purchasing managers' index remains above the 50 level that signifies growth, but the reading has fallen for two straight months, evidence of the slowing momentum.

That slowing momentum recently led Vanguard to cut its full-year forecast for China growth from 9% to just above 8.5%.

Emerging markets

Virus resurgence, particularly in emerging Asia, has slowed first-half 2021 growth. Vanguard remains optimistic that emerging markets will post full-year 2021 growth above 6%, which is above consensus.

We believe that emerging markets could get a bounce in 2022, as well, from strengthening developed markets.

Our view depends to no small degree on the pace to which emerging markets can accelerate their vaccination efforts.

A strong but uneven global recovery

The degree to which economic activity can resume depends on the staying power of COVID-19 and its variants.

Vaccination progress suggests an uneven global economic recovery. Consumers are more likely to engage in face-to-face economic activity where vaccination rates are greatest.

Emerging markets remain at greater risk from COVID-19 and its variants than developed markets given the pace of vaccinations.

Persistent inflation remains a risk

Prospects for stimulative fiscal policy and only a gradual readjustment of a supply-and-demand imbalance increase the likelihood of moderately higher inflation more persistently. We don't, however, foresee a return to 1970s-style runaway inflation. There is a risk that significantly more fiscal spending on the order of $2 trillion to $3 trillion—our "go big" scenario in the chart below—could lead inflation to significantly overshoot the Fed's target later this year and into 2022.

The Consumer Price Index (CPI) in the United States rose by a greater-than-expected 0.9% in June compared with May, and 5.4% since June 2020, the U.S. Bureau of Labor Statistics reported Tuesday, July 13.

The rises were the greatest for both readings since 2008. Core CPI, which excludes volatile food and energy prices, rose 0.9% compared with May and 4.5% compared with June 2020.

The index for used cars and trucks, up 10.5% in June, accounted for more than a third of the seasonally adjusted all-items increase.

Vanguard sees a risk that inflation could be more persistent if sectoral drivers of inflation remain strong. The Federal Reserve's preferred measure of inflation, the core Personal Consumption Expenditures Price Index (PCE), moderated somewhat in May, rising 0.4% compared with a month earlier after a revised 0.6% gain in April.

Compared with a year earlier, core PCE increased by 3.9% in May, higher than the 3.6% increase in April.

Vanguard expects year-on-year readings of core PCE to remain above 2% into 2022 amid supply constraints that could push sector-level prices higher.

Fed likely to remain dovish

We foresee accommodative policy remaining in place the rest of the year, though talk of reducing the pace of asset purchases will ramp up in the second half. We don't foresee conditions meeting the Federal Reserve's rate-hike criteria until the second half of 2023.

The U.S. Federal Open Market Committee (FOMC) voted on June 16 to leave the target range for its federal funds rate unchanged at 0%–0.25% and its bond-buying program unchanged. A survey of FOMC members, however, suggested the Fed now foresees the timing of its first post-pandemic rate hikes in 2023, rather than in 2024 as per the previous survey, in March.

Vanguard expects the Fed's balance sheet guidance to ramp up in the second half of 2021 amid economic uncertainty that remains high.

We expect policy largely to remain dovish, with the Fed tolerating above-target inflation over the medium term.

Globally, we find that central bank policy rates and interest rates more broadly are likely to rise, but only modestly, in the next several years.

Our view that lift-off from current low policy rates may occur in some cases only two years from now reflects, among other things, an only gradual recovery from the pandemic’s significant effect on labor markets.

Alongside rises in policy rates, Vanguard expects central banks, in our base-case "reflation" scenario, to slow and eventually stop their purchases of government bonds, allowing the size of their balance sheets as a percentage of GDP to fall back toward pre-pandemic levels.

We expect higher policy rates and smaller central bank balance sheets to cause only a modest lift in yields.

Unemployment rate expected to fall

The job market in the United States gained momentum in June, as 850,000 non-farm jobs were created.

Vanguard expects monthly job gains to average around 650,000 for the rest of the year, and for the unemployment rate, currently at 5.9%, to fall toward the mid-4% range by year-end.

In the leisure and hospitality sector, job-churning (workers' leaving one employer for another) is at 20-year highs amid fierce labor competition. We see that situation normalizing in the months ahead.

Labor force dynamics could change noticeably around September as enhanced unemployment benefits and CARES Act unemployment coverage of workers not traditionally covered expire, as schoolchildren return to classrooms allowing parents to return to workplaces, and as vaccination rates near their peak.