Is Inflation Reaccelerating?

It would likely take an extraordinary change in the data to bring a June cut back on the table, but the Fed’s path thereafter is still to be determined, and remains reliant on how inflation progresses from here.

So far this year, the last mile of disinflation has proven to be the hardest. CPI inflation has been accelerating, Core PCE inflation surprisingly rose in 1Q24, and the Employment Cost Index (ECI) climbed a stronger-than-expected 1.2%—its largest gain in a year. Even the trimmed mean PCE, which strips out the most volatile components in the basket, was higher in March than any month in 4Q23. This has raised questions about whether the path to 2% inflation is still encountering “bumps” along the road, or a more problematic trend higher.

Sticky price pressures pose a challenge for the data-dependent Fed, casting doubt on the possibility of any rate cuts this year. Indeed, it would likely take an extraordinary change in the data to bring a June cut back on the table, but the Fed’s path thereafter is still to be determined, and remains reliant on how inflation progresses from here.

Fortunately, a look across the drivers of inflation offer several reasons why a significant reacceleration of inflation is unlikely:

Wages may be sticky, but a labor market cooldown is underway. Labor supply has seen a welcome improvement with the recent migrant surge, building labor force participation and steadying job turnover (i.e. quits rate). Moreover, business surveys indicate cooling labor demand (NFIB and PMIs) and consumer surveys show workers are more concerned about job security. While this week’s jobs print may be strong, strong job growth is not an issue for the Fed so long as wage gains remain stable and labor tightness eases.

Consumers are more price sensitive now. The inflation surge of 2022 was driven by supply bottlenecks combined with pent-up consumer demand, whereas the consumer today is much more quiescent. Spending levels are overall quite healthy (at least in nominal terms), but there is heightened price sensitivity amongst consumers leading to trade-downs and weakness in discretionary spending. The consumer remains resilient, but it is not exuberant.

Inflation expectations are well anchored. Long-term inflation expectations from consumers, professional forecasters and bond markets are averaging 2.4%, just slightly higher than the 10yr average of 2.3%.

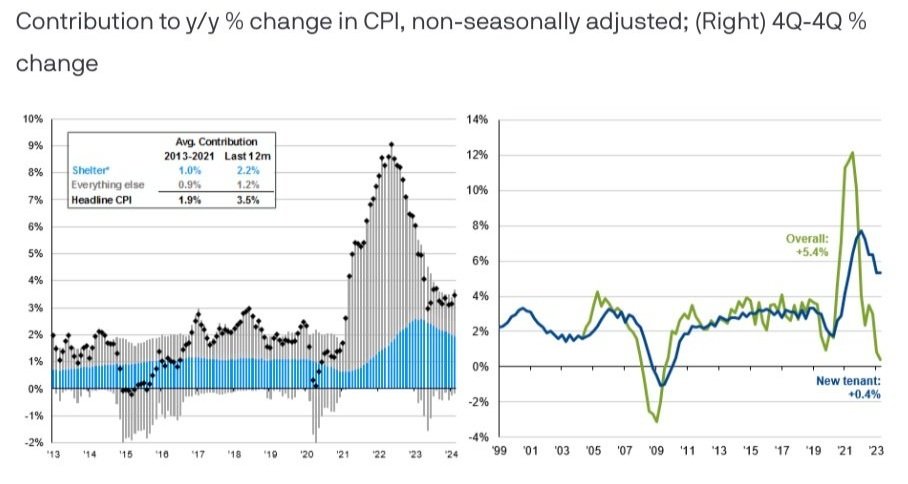

The pace of shelter inflation is unsustainable. There are two main reasons why CPI lags and dilutes swings in market rent inflation: (1) CPI rents reflect average rent growth for all tenants, in contrast to market measures like Zillow and Apartment List that capture new leases signed on rental units (2) the BLS only examines rents every six months and attributes one-sixth of the total observed increase to the month, smoothing out large swings. This, combined with the fact that new tenant leases only make up 9% of the market, suggest that while market rents fell dramatically over the course of 2022-2023, the passthrough to CPI has been limited and its lagging more than expected. Still, in absolute terms, shelter accounts for more than double its typical contribution to CPI and the New Tenant Rent Index[1], Zillow and Corelogic all suggest CPI rent inflation should decline over 2024 and 2025.

Overall, it seems unlikely inflation can sustain a reacceleration and much more probable that disinflation will resume in the coming months. In the meantime, PCE inflation of 2.7% y/y is not cause for alarm. The economy remains strong, workers are fully employed and experiencing real wage gains, and markets have shown resilience in handling higher-for-longer rates. While the Fed’s cutting cycle may be delayed, the risk of “stagflation”, where rising inflation is paired with weak growth, does not seem significant at this time.

Shelter accounts for 2x its normal inflation contribution, but the BLS's rent price gauge suggest cooler prints are ahead

Source: BEA, BLS, Cleveland Fed, FactSet, J.P. Morgan Asset Management. (Left) *"Shelter" does not include the category for hotel lodging. (Right) Chart shows the "New Tenant Rent Index" and the "All Tenant Regressed Rent Index" from the BLS and Cleveland Fed. These indices use a repeat rent methodology which, compared to the CPI-Rent of Primary Residence Index that uses a weighted average of the sixth root of changes in economic rent, mitigates bias from sample composition changes. See https://www.bls.gov/pir/new-tenant-rent.htm for full details. Data are as of April 30, 2024.

[1] The New Tenant Rent Index is a new experimental index from the BLS and Cleveland Fed that applies a similar method as the Zillow index to the CPI Housing survey by tracking market rents only with observations in the CPI dataset that follow a change in tenant. Full methodology details can be found here: https://www.bls.gov/pir/new-tenant-rent.htm