Market Week: September 8, 2020

The Markets (as of market close September 4, 2020)

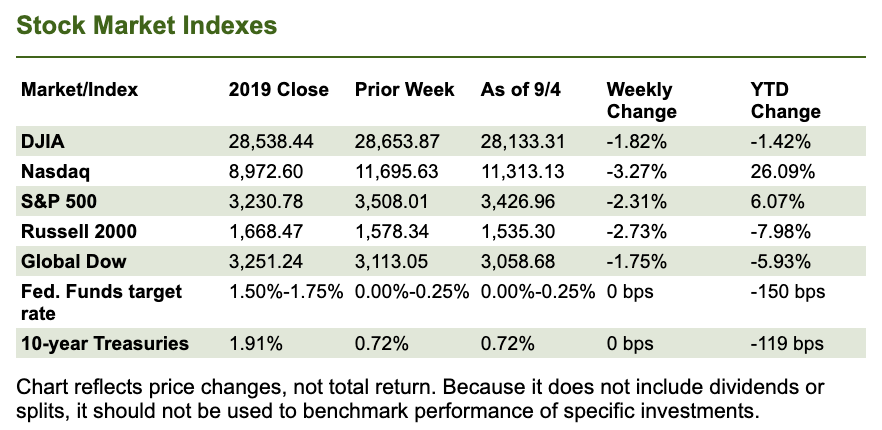

Stocks sagged last Monday, but not enough to dampen a banner month of returns in August. Only the Nasdaq pushed ahead to start the week as the remaining benchmark indexes lost value. Crude oil prices, Treasury yields, and the dollar all declined.

Last Tuesday marked the first day of September and the start of another strong market performance. Each of the benchmark indexes listed here posted solid gains, led by the Nasdaq (1.4%), the Russell 2000 (1.1%), the Dow (0.8%), the S&P 500 (0.8%), and the Global Dow (0.1%). Rising bond prices drove Treasury yields lower. Crude oil prices and the dollar rose. Surging mega-caps gave the market a boost, as did materials, technology, and communications.

Wednesday saw both the S&P 500 and the Nasdaq soar to fresh record highs. Utilities and financials led the way while technology shares lagged. The dollar rose while crude oil and Treasury yields dropped. Global stocks also surged last Wednesday as investors anticipated further stimulus (and liquidity) from central banks.

Last Thursday, in a complete reversal, stocks suffered their worst day since June. The Nasdaq plunged 5.0%, the S&P 500 dropped 3.5%, the Russell 2000 gave back 3.0%, the Dow fell 2.8%, and the Global Dow lost 1.7%. Money moved to Treasuries sending bond prices higher and yields plummeting. Crude oil prices fell and the dollar rose. Mega-caps and technology stocks sank, pulling the major market indexes lower. Analysts have been pointing to overvaluations in some sectors, particularly technology, and investors may be taking heed.

Tech shares continued to tumble last Friday, pulling the Nasdaq down to its worst week since March. The selloff that began last Thursday continued into Friday as each of the benchmark indexes listed here lost value on the last day of the week. Treasury yields climbed, the dollar fell, and crude oil prices fell below $40 per barrel. Mega-caps tumbled again last Friday as investors continue to show concern that the market may be overvalued.

For the week, early gains weren't enough to overcome losses later, as each of the indexes listed here lost value. The Nasdaq fell 3.3%, followed by the Russell 2000 (-2.7%), the S&P 500 (-2.1%), the Dow (-1.8%), and the Global Dow (-1.8%). Even favorable employment data wasn't enough to halt the selloff. An additional 1.4 million new jobs were added in August, and the latest unemployment figures showed the total number of claimants dipped below 1 million.

Crude oil prices ended the week below $40.00 per barrel, closing at $39.59 per barrel by late Friday afternoon, down from the prior week's price of $42.97. The price of gold (COMEX) also dropped last week, closing at $1,940.60, down from the prior week's price of $1,972.80. The national average retail price for regular gasoline was $2.222 per gallon on August 31, $0.040 higher than the prior week's price but $0.341 less than a year ago.

Last Week's Economic News

There were 1.4 million new jobs added in August, below the February level by 11.5 million, or 7.6%. The unemployment rate fell 1.8 percentage points to 8.4%, and the number of unemployed persons decreased by 2.8 million to 13.6 million. Nevertheless, both the unemployment rate and the number of unemployed persons remain much higher than their pre-pandemic February figures of 4.9% and 7.8 million, respectively. The labor force participation rate increased by 0.3 percentage point to 61.7% in August but is 1.7 percentage points below its February level. The employment-population ratio rose by 1.4 percentage points to 56.5% but is 4.6 percentage points lower than in February. In August, 24.3% of employed persons teleworked because of the coronavirus pandemic, down from 26.4% in July. In August, 24.2 million persons reported that they were unable to work because their employer closed or lost business due to the pandemic — down from 31.3 million in July. Government employment rose in August, largely reflecting temporary hiring for the 2020 Census. Notable job gains also occurred in retail trade, professional and business services, leisure and hospitality, and education and health services. In August, average hourly earnings rose by $0.11 to $29.47. The average work week increased by 0.1 hour to 34.6 hours in August.

Manufacturing continues to recover from the slowdown brought about by the COVID-19 pandemic. According to the August Manufacturing ISM® Report On Business®, manufacturing expanded for the fourth consecutive month. New orders, production, employment, prices, exports, and imports all advanced in August over July. Inventories were lower, the result of an acceleration of shipments and deliveries.

The services sector grew in August, but at a slower place than July, according to the latest Services ISM® Report On Business®. Business activity and production fell in August, as did new orders and inventories. Employment, supplier deliveries, prices, backlog of orders, exports, and imports each increased last month.

The trade deficit increased by $10.1 billion in July, according to the latest report from the Bureau of Economic Analysis. July exports were $12.6 billion more than June exports. July imports were $22.7 billion more than June imports. Year to date, the goods and services deficit increased $6.4 billion, or 1.8%, from the same period in 2019. Exports decreased $257.8 billion, or 17.5%. Imports decreased $251.3 billion, or 13.8%. The deficit with Mexico increased $2.5 billion in July, and the deficit with China increased $1.6 billion. The United States had a trade surplus with South America and Central America ($2.9 billion), OPEC ($1.5 billion), Hong Kong ($1.4 billion), and the United Kingdom ($0.6 billion).

For the week ended August 29, there were 881,000 new claims for unemployment insurance, a decrease of 130,000 from the previous week's level, which was revised up by 5,000. According to the Department of Labor, the advance rate for insured unemployment claims was 9.1% for the week ended August 22, a decrease of 0.8 percentage point from the prior week's rate. The advance number of those receiving unemployment insurance benefits during the week ended August 22 was 13,254,000, a decrease of 1,238,000 from the prior week's level, which was revised down by 43,000.

Eye on the Week Ahead

Economic reports during the Labor Day week focus on inflation, which has been muted at best. Both the Producer Price Index and the Consumer Price Index for August are out this week. Producer prices advanced 0.6% in July, but are down 0.4% over the last 12 months. Consumer prices also inched ahead by 0.6% in July and have increased a scant 1.0% for the year.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.