Market Week: July 27, 2020

The Markets (as of market close July 24, 2020)

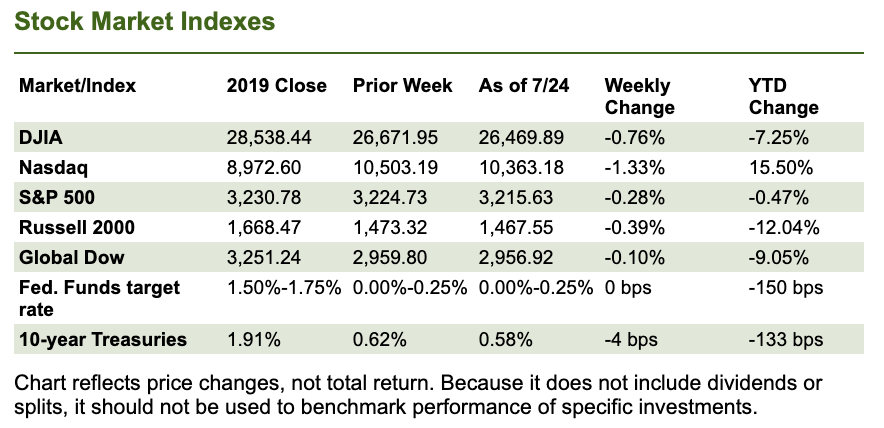

Last week started off on a high note as stocks reached levels not seen since February. The Nasdaq gained 2.5% last Monday, led by a surging Amazon and Zoom Technologies soared to a record high following the publication of positive COVID-19 vaccine results. Investors were encouraged by signs out of Washington that additional stimulus was on the way. The S&P 500 advanced 0.8% on the day while the Dow's gain was negligible.

The Russell 2000 recovered from a poor Monday by gaining 1.3% last Tuesday to lead the benchmark indexes listed here. The Global Dow rose 0.9%, buoyed by a new round of economic stimulus from the European Union. The Dow climbed 0.6%, and the S&P 500 inched up 0.2%. The Nasdaq retreated from its record high on Monday, giving back 0.8% last Tuesday.

Wednesday saw equities rise despite an increase in tensions between the United States and China. Pfizer vaulted 5.1% on positive COVID-19 vaccine developments. The Dow and the S&P 500 each gained nearly 0.6%, with the latter reaching a five-month high. The Nasdaq and the Russell 2000 each gained 0.2% on the day.

Stocks ended a 4-day run last Thursday, falling to their lowest levels in a week. An unanticipated rise in unemployment claims and lower-than-expected earning reports from some major tech companies contributed to the decline. Stock prices fell for some of the major market players including Amazon, Alphabet (Google), Facebook, Microsoft, Apple, and Tesla. The Nasdaq plunged 2.3% followed by the Dow, which fell 1.3%. The S&P 500 dropped 1.2%. Crude oil prices, the dollar, and Treasury yields all declined.

Equities ended last week on a sour note with each of the indexes listed here losing value. The Russell 2000 dropped 1.5% on the day, followed by the Nasdaq (-0.9%), the Dow (-0.7%), the Global Dow (-0.7%), and the S&P 500 (-0.6%). Investors seemed concerned over escalating discord between the United States and China, disappointing earnings reports, and the likelihood of more fiscal stimulus.

Last week saw the run of solid market gains end as each of the benchmark indexes listed here posted losses. The Nasdaq, which had strung together several weeks of gains, fell back for the second consecutive week. The large caps of the Dow and the S&P 500 also lagged after advancing for three consecutive weeks. Year-to-date, the Nasdaq is still well ahead of its 2019 closing value, while the S&P 500 is within 0.5% of breaking even. The Dow, Global Dow, and Russell 2000 remain well off their respective 2019 closing marks.

Crude oil prices ended the week at $41.18 per barrel by late Friday afternoon, up from the prior week's price of $40.58. The price of gold (COMEX) advanced for the sixth consecutive week, closing at $1,899.60, up from the prior week's price of $1,812.20. The national average retail price for regular gasoline was $2.186 per gallon on July 20, $0.009 lower than the prior week's price and $0.564 less than a year ago.

Last Week's Economic News

Sales of existing homes rebounded in June following declines in March, April, and May. According to the latest report from the National Association of Realtors®, total home sales jumped 20.7% last month from May. However, existing home sales are 11.3% below their pace of a year ago. The median existing-home price for all housing types in June was $295,300 ($284,600 in May), up 3.5% from June 2019. Total inventory is up 1.3% in June and sits at a four-month supply. Sales of existing single-family homes also surged in June, climbing 19.9% from May. Single-family home sales are down 9.9% from a year ago. The median existing single-family home price was $298,600 in June, up 3.5% from June 2019.

New single-family home sales also surged in June, climbing 13.8% above May's totals. Sales of new single-family homes are 6.9% above the June 2019 estimate. The median sales price of new houses sold in June 2020 was $329,200. The average sales price was $384,700. Inventory of new single-family homes for sale in June was 307,000, representing a 4.7-month supply at the current sales rate.

For the week ended July 18, there were 1,416,000 claims for unemployment insurance, an increase of 109,000 from the previous week's level, which was revised up by 7,000. According to the Department of Labor, the advance rate for insured unemployment claims was 11.1% for the week ended July 11, a decrease of 0.7 percentage point from the prior week's revised rate. The advance number of those receiving unemployment insurance benefits during the week ended July 11 was 16,197,000, a decrease of 1,107,000 from the prior week's level, which was revised down by 34,000.

Eye on the Week Ahead

The last week of July will focus on the first estimate for the second-quarter gross domestic product. The GDP decreased 5.0% in the first quarter of 2020. The June report on personal income and spending is out at the end of the week. Not unexpectedly, personal income fell 4.2% in May, but consumer spending increased 8.2%. The June tally should show better numbers for income, as many businesses ramped up operations last month.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.